Hospitality Insurance Claim: Key Findings

- The top restaurant claim categories are equipment breakdown (17%), employee injuries (12.9%) and slip-and-falls (12.8%).

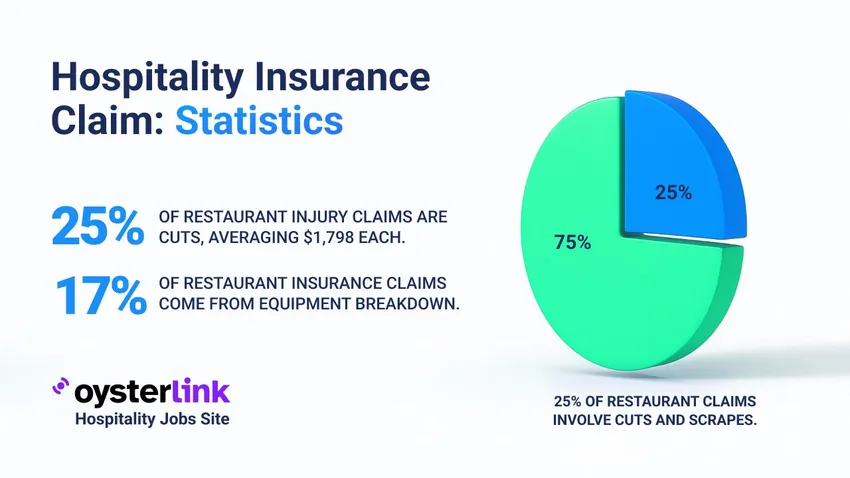

- Cuts make up 25% of restaurant injury claims ($1,798 average), while fractures represent just 3% but cost $22,837 each.

- Hotel insurance costs rose 19.5% in 2023, now consuming 1.7% of revenue and averaging $939 per available room.

A hospitality insurance claim is a formal request by a business in the sector, such as a restaurant or hotel, to cover financial losses from accidents, injuries or property damage.

This article shares the latest statistics showing which claims are most common, how much they cost and the broader trends shaping insurance expenses in hospitality.

Types of Hospitality Insurance Claims

These figures highlight the most common claims in hospitality, their frequency, average costs and seasonal trends.

- Cuts are the most frequent restaurant injury claim, making up roughly one-quarter of reported cases. They tend to be minor, averaging $1,798 per claim.

- Fractures represent only 3% of claims but carry the highest price tag, averaging $22,837 per case.

- Strains account for about 8% of claims (over 10,000 cases) and average $10,672 each, making them financially significant due to both frequency and cost.

The Fastest Growing

Restaurant & Hospitality Job Platform

Looking for top paid jobs? Or Hiring for your business?

- Slip-and-fall incidents generate 4.5 times higher payouts than cuts or punctures, showing how costly these accidents are in restaurant settings.

- Between January 2021 and July 2024, five categories made up the bulk of restaurant insurance claims: equipment breakdown, employee injuries, customer slip-and-falls, theft and vandalism.

- The costliest restaurant claim categories from 2021–2024 were fire, slip-and-fall, assault & battery and water damage.

- Restaurants filing an insurance claim saw an average loss of $9,000.

- Fine dining venues reported nearly double the average claim costs compared to all other restaurants.

- Claims peak during summer (June–August), the busiest period for restaurant workplace accidents.

Hospitality Insurance Claim Settlements and Policy Limits

When injuries exceed standard coverage, claims often escalate into lawsuits with significantly higher settlement ranges.

- Insurance policy limits often cap payouts, but serious injuries can exceed these amounts and result in lawsuits. In court, slip-and-fall settlements typically range from $10,000–$50,000.

- When surgery is required, settlement amounts often surpass coverage, with payouts ranging from $50,000 to more than $200,000.

- Courts often calculate pain-and-suffering damages at 1.5 to 5 times the medical costs, significantly increasing total settlement values.

The Fastest Growing

Restaurant & Hospitality Job Platform

Looking for top paid jobs? Or Hiring for your business?

Liquor Liability in Hospitality Insurance

Alcohol-related incidents are among the riskiest exposures in the industry, with premiums and payouts heavily influenced by state laws.

- Businesses generating more than 50% of revenue from alcohol sales face greater difficulty obtaining liquor liability coverage.

- Coverage limits drive premium size: restaurant owners usually set $1 million limits, while bars often choose $2 million.

- The average monthly premium for liquor liability insurance is about $45 (≈$542 annually).

- A majority (52%) of policyholders spend less than $50 per month on this coverage.

- In states with stricter dram shop/liquor liability rules, businesses with ≤$1.5M in alcohol sales can face six-figure minimum premiums because of high claim severity.

- In South Carolina, minimum liquor liability premiums have risen to about $100,000, reflecting claim history and settlements.

- Liquor liability has proven unprofitable, with insurers losing about $2.60 for every $1 collected in premiums.

- Establishments with past liquor-related claims have seen premiums jump by 300%–400%, underscoring how loss history directly impacts costs.

The Fastest Growing

Restaurant & Hospitality Job Platform

Looking for top paid jobs? Or Hiring for your business?

Hotel Insurance Claims and Cost Trends

Hotels face mounting insurance costs, with claim activity tied to property damage, liability, and regional risks such as hurricanes and wildfires.

- Hotel insurance expenses rose 19.5% in 2023, driven largely by rising claim costs, making insurance one of the fastest-growing expenses for operators.

- Claims now consume about 1.7% of hotel operating revenue, compared with a long-term average of 1.2%.

- In 2022, insurance averaged $939 per available room (PAR), with resorts at $2,464 PAR and limited-service hotels at $528 PAR.

- Premiums vary by region: hotels in the Southeast grew at a 7.2% CAGR, and Mountain/Pacific hotels at 6.2%, reflecting exposure to hurricanes, wildfires and other natural disasters.

- From 2015–2022, hospitality insurance costs increased at an annual rate of 6.2%, highlighting long-term claims growth.

- Between 2019 and 2021, hotel revenues fell 40%, yet insurance expenditures rose 33.1%.

- In 2021, average hotel insurance spending was $784 PAR, compared with $2,224 for resorts and just $413–$482 for extended-stay and limited-service properties.

- Certain regions, including Mountain/Pacific and South Atlantic, recorded the sharpest cost increases, while New England/Mid-Atlantic saw a 1.7% decline.

Check Our Career Growth Tools

Other Insurance Exposures Affecting Hospitality Claims

Businesses also face exposure to risks like cyberattacks, lawsuits or rising liability costs.

- The average cost of a data breach in hospitality reached $3.36 million in 2023, up 14% from the prior year.

- Scattered Spider, the group behind the 2023 MGM and Caesars breaches, still targets hospitality; threat frequency is 3.92 in the U.S. vs. 1.91 in the U.K., showing higher U.S. exposure.

- General liability premiums for hospitality businesses are up 5%–25%, depending on claims history.

- Umbrella and excess liability premiums climbed 9.5% in Q1 2025, following an 8.7% increase in Q4 2024. Hospitality is rising faster than average due to frequent guest-related claims.

- Property insurance rates for hospitality businesses are increasing by 17%–26%, with high-risk or loss-heavy properties facing hikes of 50% or more.

- Workers’ compensation premiums show mixed results: overall, market averages fell 2.6%, but claim-heavy hospitality operators experienced 30%–40% increases.

Underinsurance in the Hospitality Industry

Alongside rising claims and premiums, another major risk for hospitality operators is underinsurance.

While U.S.-specific statistics are limited, figures from Australia and the UK highlight how severe and widespread the issue can be in the hospitality sector.

- In Australia, about 80% of property owners and 62% of SMEs are underinsured, leaving many hospitality businesses vulnerable.

- One Australian hotel saw its payout reduced by 50% when the insurer applied a co-insurance clause due to underinsurance.

- In the UK, 40% of businesses said lack of insurance knowledge is the main reason for being underinsured.

- Another 35% blamed not reviewing policies often enough.

- 19% attributed underinsurance to higher material costs and 7% to operational changes.

- More than 40% of UK commercial properties are underinsured.

Post a Hospitality Job on OysterLink

In addition to providing detailed reports and real-time data, OysterLink allows hospitality employers to connect with top hospitaltiy job seekers.

Posting a job on OysterLink is simple and affordable. With over 350,000 monthly active users, finding hospitality talent has never been easier.

The Fastest Growing

Restaurant & Hospitality Job Platform

Looking for top paid jobs? Or Hiring for your business?

Loading comments...