If you’re a Private Chef, pop-up Bartender, freelance caterer, or any gig-based hospitality worker, taxes can be confusing. One crucial area you can’t afford to ignore is Social Security tax.

Independent contractors must handle Social Security and Medicare taxes themselves, and skipping these steps can hurt you now and in the long run.

The good news? With a clear plan, you can stay on top of your Social Security obligations. Let’s break down exactly what you need to do to cover your Social Security taxes as a 1099 worker in hospitality.

Understand Your Social Security Tax Obligations as a 1099 Worker

When you work a traditional job, your employer withholds FICA taxes (Federal Insurance Contributions Act) from your paycheck for Social Security and Medicare, and the employer matches those contributions.

But as an independent contractor, you’re responsible for the whole thing yourself. In fact, self-employed people pay Self-Employed Contributions Act (SECA) taxes, which fund Social Security and Medicare just like FICA taxes do.

This self-employment tax is essentially both the employee and employer share combined.

For 2025, the self-employment tax rate is 15.3% of your net earnings.

This rate has two parts: 12.4% for Social Security (officially covering old-age, survivors, and disability insurance) and 2.9% for Medicare.

In other words, you’re paying the equivalent of 6.2% + 6.2% for Social Security (both halves) and 1.45% + 1.45% for Medicare. It might sting to pay that much, but it’s the trade-off for being your own boss. The key is understanding that no one else is withholding these taxes for you – it’s on you to calculate and pay them.

Why Paying Into Social Security Matters for Your Future

It’s tempting in the hospitality industry to deal in cash and forget about taxes. But paying Social Security tax is what builds your eligibility for Social Security benefits later on. The Social Security Administration tracks your earnings over your working life. If you don’t report income and pay in, you won’t earn the “credits” needed to qualify for benefits. In fact, “we cannot pay benefits if you don’t have enough credits,” the SSA warns

Generally, you need about 10 years of work (40 credits) to be eligible for Social Security retirement benefits (fewer years for disability, depending on your age).

Every year that you earn income and pay self-employment tax, you accumulate credits. In 2025, for example, one credit is earned per $1,810 of earnings, up to 4 credits per year.

If you never pay in (or under-report your earnings), you’re shrinking your future retirement check and risking your access to disability protection.

Hospitality work can be physically demanding – paying into Social Security also means you could qualify for disability benefits if you get seriously hurt or ill and can’t work.

Bottom line: 1099 income directly impacts your Social Security benefits. Don’t shortchange yourself in the long run by skipping these taxes now.

Report All Your Gig Income (Yes, Even Cash Tips)

The first step is making sure you report all the income you earn from your hospitality gigs. Whether you get paid by check, through a payment app, or cash at the end of the night, it’s all taxable income.

Many hospitality contractors will receive a Form 1099-NEC from clients who paid them $600 or more in a year. But even if a client doesn’t send you a 1099 (for example, if you made $500 at an event), you are still required to report that income on your tax return. The IRS considers it self-employment or business income.

Keep a log of every gig: the date, who you worked for, and how much you earned (including any tips or service fees you kept). Good recordkeeping ensures nothing slips through the cracks.

Why so strict? Because if you underreport your earnings, you’re not only risking IRS penalties, you’re also not getting credit for that work toward Social Security. In short, if you worked it, report it.

(One small exception: if your net self-employment earnings for the entire year are under $400, you generally don’t owe self-employment tax – more on that next.) But if you made at least $400 net from your combined gigs, you must file a return including Schedule SE to pay Social Security tax.

Know the $400 Rule and Calculate Your Net Earnings

Not every side hustle dollar ends up taxed for Social Security – very small amounts might be exempt. The IRS says that if your net earnings from self-employment were $400 or more for the year, you must pay self-employment tax and file Schedule SE.

“Net earnings” means your profit after business expenses. For example, if you earned $5,000 bartending private events, but had $1,000 of related expenses (maybe supplies or travel), your net self-employment income is $4,000. That $4,000 is what the 15.3% tax applies to. (If your net came out to less than $400 total, you wouldn’t owe Social Security/Medicare tax – however, such low earnings also mean you might not earn a credit for Social Security that year.)

To figure out your net earnings, you’ll usually fill out Schedule C (Profit or Loss from Business) as part of your Form 1040. This is where you list your income and any deductible expenses from your hospitality work.

The resulting net profit (or loss) then flows into your Form 1040 and is used on Schedule SE to calculate your Social Security and Medicare taxes. The 15.3% self-employment tax applies to net earnings above $400 in a year.

If you have a loss or very low profit, you might not owe self-employment tax at all (though you still file the forms). Most independent bartenders, chefs, and gig workers, however, will cross that threshold in a busy year.

Use Schedule SE (Form 1040) to Figure Your Social Security Tax

Once you know your net earnings, it’s time to compute the self-employment tax on Schedule SE, which is filed with your Form 1040. Schedule SE is the form that “helps you take your net earnings and apply the 12.4% Social Security tax as well as the 2.9% Medicare tax”.

In practice, the form will walk you through multiplying your annual net self-employment income by 92.35% (this adjustment allows for the deductible half of SE tax) and then applying the 12.4% and 2.9% rates. Don’t worry – tax software or your tax preparer will handle the calculations, but it’s good to understand what’s happening behind the scenes.

A couple of important points to note while filing Schedule SE:

- Social Security Wage Base: Social Security tax (12.4%) only applies up to an annual income limit. For example, in 2024 the first $168,600 of combined wages and self-employment earnings is subject to Social Security tax. Most hospitality contractors won’t hit that cap, but if you also have a high-paying day job or a very successful business, just be aware there is an upper limit each year.

- Medicare Tax: The 2.9% Medicare portion has no income cap – all your net earnings are taxed for Medicare. Additionally, high earners may owe an extra 0.9% Medicare surtax over $200k (single) but again, this likely won’t affect the average freelancer chef or bartender.

- Half of SE Tax is Deductible: The IRS lets you deduct 50% of your self-employment tax when calculating your adjusted gross income, to reflect the “employer” half. This won’t reduce the self-employment tax you owe, but it will lower your income tax a bit. Schedule SE and your 1040 instructions will handle this deduction automatically.

After crunching the numbers, Schedule SE will show your total self-employment tax due. This amount ultimately gets transferred to your Form 1040 (on the line for “Self-Employment Tax”) and added to your income tax liability.

It’s important to file Schedule SE along with your 1040 by tax day (April 15) if you had $400+ in net self-employment income, even if you might otherwise not owe much income tax. The Social Security Administration uses the info from Schedule SE to credit your Social Security earnings record. So failing to file it means no credit for that work!

Set Aside Money from Each Gig for Taxes

One practical strategy for self-employed hospitality workers is to set aside a portion of each payment you receive for taxes. Since no employer is withholding taxes for you, you should act as your own HR department in a sense. A common rule of thumb is to put aside around 25–30% of every payment you get from a client for taxes.

This chunk accounts for your 15.3% self-employment (Social Security/Medicare) tax plus some buffer for federal (and possibly state) income taxes. For instance, if you cater a wedding and earn $1,000, try to immediately set aside about $250–$300 in a separate savings account earmarked for taxes. That way, you won’t be caught short when tax time comes.

In addition, keep a running total of your income and expenses. Use a simple spreadsheet, a notebook, or an expense tracking app – whatever you will actually maintain. Every time you finish a gig, log the income (and any related expenses like ingredients, gas mileage, or equipment).

This not only makes tax filing easier, but it also helps you estimate how much you should be saving for taxes as the year goes on. If you notice a big seasonal influx (say you made most of your money in summer event season), plan ahead to save more during those high-earning months.

Being disciplined about setting aside money will save you from scrambling or going into debt to pay a tax bill later. It’s all about making the “tax bite” feel less painful by spreading it out through the year.

Pay Quarterly Estimated Taxes to Avoid IRS Penalties

The U.S. tax system is “pay-as-you-go,” meaning the IRS expects you to pay taxes throughout the year as you earn income.

For traditional employees, this happens automatically via paycheck withholding. But as a self-employed worker with no withholding, you likely need to pay quarterly estimated taxes. In fact, generally if you expect to owe at least $1,000 in tax when you file, you should be making estimated tax payments during the year.

Most independent contractors fall in this category, especially if your hospitality gigs are a primary source of income.

Quarterly tax payments break up your tax bill into four installments, due on April 15, June 15, September 15, and January 15 of the following year (dates can shift slightly if they fall on weekends/holidays).

These payments cover your self-employment tax and any income tax that will be due on your profits. By paying in quarterly, you accomplish two things:

- Avoiding Surprises: You won’t face one giant tax bill in April because you’ve been chipping away at it all year.

- Avoiding Penalties: The IRS charges penalties and interest if you underpay your taxes during the year. You can dodge these penalties by paying enough through the year – usually at least 90% of your current year tax owed by year-end (or 100% of last year’s tax, as a safe harbor)

To figure out how much to pay each quarter, you can use Form 1040-ES (Estimated Tax for Individuals), which includes worksheets to calculate your expected tax. Essentially, you’ll estimate your net earnings for the year, compute the tax (15.3% SE tax + income tax), then divide into four payments.

Don’t worry if your income isn’t perfectly even each quarter – pay your best estimate. It’s better to pay something regularly than to fall behind. The IRS also offers convenient ways to pay: you can mail in a 1040-ES voucher with a check, or pay online via IRS Direct Pay or the Electronic Federal Tax Payment System.

Mark the quarterly due dates on your calendar so they don’t sneak up on you. If your income fluctuates, you can adjust the payment amounts later (there are provisions to annualize income if needed). The main goal is to pay as you go, so you won't owe a big lump sum

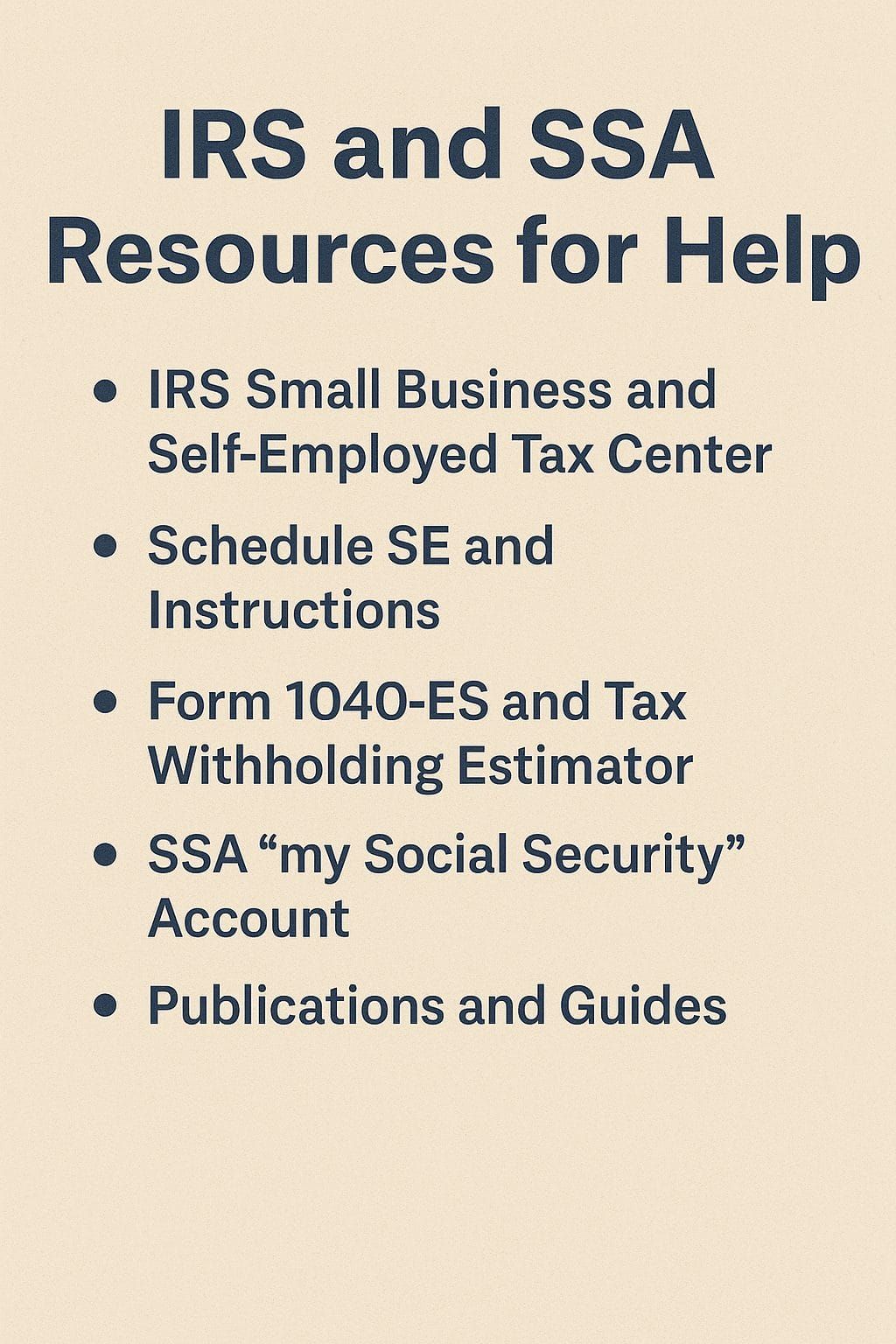

Tap Into IRS and SSA Resources for Help

You’re not alone in figuring all this out – both the IRS and the Social Security Administration provide free tools and resources for self-employed workers. Here are a few highly useful ones:

- IRS Small Business and Self-Employed Tax Center: The IRS’s online hub for self-employed individuals has information on when and how to file, links to forms, and answers to common questions【13†】. It’s a good starting point for official guidance.

- Schedule SE and Instructions: If you want to see the form that calculates your Social Security tax, check out Schedule SE (Form 1040) on the IRS website. The IRS also provides detailed instructions and examples to help you fill it out correctly.

- Form 1040-ES and Tax Withholding Estimator: To plan your quarterly payments, Form 1040-ES includes worksheets, and the IRS’s online Tax Withholding Estimator tool can help approximate your needed payments. These tools can prevent underpaying or overpaying during the year.

- SSA “my Social Security” Account: Create an account on SSA.gov to track your earnings record and see your estimated future benefits. This is a great reality check – it shows you how your reported income (including self-employment) translates into retirement dollars. Seeing a $0 for a year of no reported income might motivate you to always file and pay the SE tax! Remember, your 1099 income only counts toward Social Security if you report it.

- Publications and Guides: IRS Publication 334 (Tax Guide for Small Business) and the SSA’s pamphlet If You Are Self-Employed are useful reads. They cover the basics of reporting business income, deductions, and paying self-employment tax, all in plain language with examples.

Finally, don’t hesitate to get professional advice if your situation is complex. A tax professional who understands the gig economy or hospitality industry can help you maximize deductions (to reduce income tax) while making sure you’re still contributing enough for Social Security.

The goal is to be realistic and proactive: hospitality income can be irregular, but your tax responsibilities are steady. By following these steps – understanding your obligations, tracking your income, setting aside money, filing the right forms, and paying taxes quarterly – you’ll stay out of trouble with the IRS and secure your future Social Security benefits.

In a business where you take care of everyone else (serving guests and clients), don’t forget to take care of yourself by not skipping these Social Security tax steps. Your future self will thank you!

Loading comments...