The restaurant business is tough. 60% of new restaurants fail in their first year, and 80% shut down within five years.

Opening a restaurant requires a major financial commitment. The average startup costs reach $275,000, and property purchases can drive this number up to $425,000.

Restaurant owners need to know their funding options. This knowledge helps both experienced restaurateurs who need extra capital and newcomers ready to start their journey.

This article explores the best sources of financial help for restaurant owners, providing insights on how to secure funding and build a sustainable business.

Financial Help for Restaurant Owners: Understanding Your Options

Restaurant owners have many financing options to choose from in 2025, making it easier to find a solution that fits their unique needs and goals.

Whether you're looking to cover immediate cash flow issues or fund long-term growth, understanding the different types of financing available is crucial.

Traditional vs alternative restaurant financing sources

Traditional bank loans and SBA programs give established restaurants better interest rates over longer periods.

SBA loans are a vital source of funding for small businesses that can't secure money elsewhere.

Online lenders and fintech platforms offer different ways to borrow money. They use smart technology to review businesses based on how well they operate rather than just their assets.

Many of these lenders can provide capital within 72 hours.

Short-term vs long-term funding solutions

Merchant cash advances and business lines of credit help restaurants handle their immediate cash needs.

A business line of credit works like a credit card, letting restaurants tap into extra funds whenever needed.

SBA loans and traditional bank financing support bigger investments like buying property or major renovations.

You'll get lower interest rates with these options, but they need more paperwork and take longer to approve.

Risk assessment for different financing types

Restaurant owners must review the specific risks that come with each financing option.

The industry's thin profit margins and high customer expectations make financial stability essential.

Your review should include changing food costs, surprise maintenance expenses and economic slowdowns.

Live analytics in finance are a great way to get ahead of these financial risks.

The Fastest Growing

Restaurant & Hospitality Job Platform

Looking for top paid jobs? Or Hiring for your business?

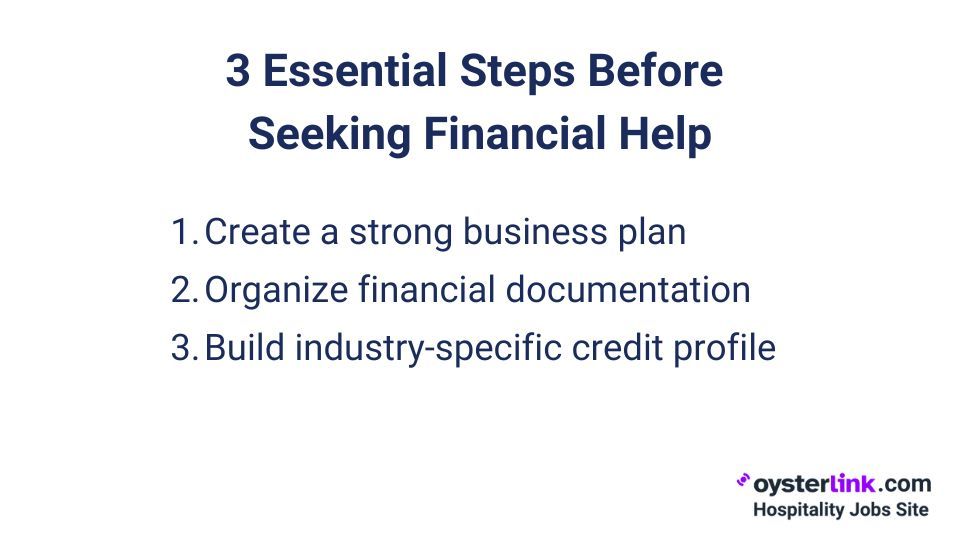

3 Essential Steps Before Seeking Financial Help as a Restaurant Owner

Strong financial preparation significantly increases your chances of securing assistance.

A well-structured plan demonstrates to potential lenders the strength and viability of your restaurant.

1. Creating a strong business plan

A comprehensive business plan is the foundation of any successful financing application.

It's often the first thing potential lenders or investors review, and it sets the tone for their decision-making process.

Your plan should:

- Clearly define your restaurant concept and what sets it apart from the competition.

- Identify your target market, including key demographics and customer segments.

- Include detailed financial projections with clear revenue goals to demonstrate profitability.

Without proper preparation, many restaurants struggle to succeed. To strengthen your business plan, ensure it also covers essential details like menu pricing, operational strategies and marketing approaches.

Collaborating with an experienced advisory team — such as an investment bank, accounting firm and legal experts — can add credibility and refine your approach.

2. Organizing financial documentation

Lenders prioritize financial stability when evaluating loan applications, so having the right documentation is essential.

Here’s what you’ll need to provide:

- Personal and business tax returns to establish your financial history.

- Bank statements from both personal and business accounts to show liquidity.

- Income statements and balance sheets to highlight your restaurant's profitability and assets.

- Current cash flow statements to demonstrate your ability to manage operational expenses.

- Accounts receivable and payable aging reports to assess how you handle debts and payments.

These documents help lenders evaluate your restaurant's financial health and your cash management skills.

Keeping your records accurate and up to date not only reflects professionalism but also builds trust with potential lenders.

3. Building industry-specific credit profile

Restaurant owners should establish a separate business credit profile to keep their personal credit intact.

Here’s how to get started:

- Register your business with Dun & Bradstreet to obtain a DUNS number, the standard for business identification.

- Build your credit profile by making small purchases with suppliers who report transactions to credit agencies.

- Monitor your business credit score, which ranges from 0–100, with a score of 75 generally seen as a strong rating by lenders.

Additionally, paying vendors and suppliers on time can positively impact your credit score and set you up for better financing terms in the future.

Establishing a solid credit profile helps you secure better funding options as your business grows.

Comparing Top Restaurant Funding Sources

The original choice of funding can significantly impact your restaurant's financial health.

Let's get into the best financing options you can find in 2025.

Bank loans and SBA programs

SBA 7(a) loans are a top choice for restaurant owners. These loans provide up to $5 million in funding with repayment terms that stretch to 25 years.

Restaurant owners can access competitive rates and substantial amounts that cover everything from real estate acquisition to equipment purchases.

Traditional bank loans come with structured payment plans and fixed monthly installments, though they're harder to secure.

Restaurant owners should have strong credit scores and detailed financial records for at least two years.

Equipment financing and merchant cash advances

Equipment financing helps restaurant owners buy essential kitchen equipment without big upfront costs. The equipment acts as collateral, which might reduce the need for additional security.

This financing option includes tax benefits and terms that match your business needs.

Merchant cash advances give quick access to capital by purchasing future credit card receivables. The repayment terms flex with your daily credit card sales.

These advances used to get pricey, but some providers now offer competitive rates for restaurant owners.

Private investors and crowdfunding platforms

Angel investors are individuals who use their personal funds to invest in early-stage businesses.

hey typically look for a 20-25% return on investment and often provide capital to startups that may not yet have access to other financing options.

Venture capitalists (VCs) are professional investors who manage pooled funds from various sources, like institutional investors.

They typically target higher returns of around 40%, as they invest in businesses with high growth potential and greater risks.

VCs often step in at later stages to help companies scale rapidly.

Private investors, such as angel investors and venture capitalists, can provide significant capital for restaurants at different stages of growth.

However, crowdfunding has emerged as a powerful alternative. It allows businesses to raise small amounts of money from a large number of people, typically via online platforms.

Crowdfunding has become an innovative financing option, with restaurant projects on platforms like Kickstarter growing from 3,400 in mid-2019 to over 4,400 by 2023.

Popular crowdfunding platforms include:

- Kickstarter: Ideal for creative restaurant concepts

- Indiegogo: Offers flexible funding options

- GoFundMe: Suitable for smaller restaurant projects

Making Smart Financial Decisions

Smart financial management requires a thorough look at funding options. Restaurant owners need to understand the total cost of each financing option to make smart decisions.

Evaluating interest rates and terms

A closer look at interest rates reveals the true cost of financing.

Fixed rates provide stability with predictable monthly payments, though they often start higher than variable rates.

Banks typically offer better interest rates for shorter loan terms, as they reward quicker repayment schedules.

Restaurant owners should consider both upfront costs and ongoing fees. While some lenders require collateral, such as business assets or personal guarantees, others focus more on your restaurant's daily operations and cash flow.

Understanding repayment schedules

Traditional financing usually runs between three to 10 years. Longer terms mean you'll pay less each month, but the total interest costs add up over time.

Alternative financing gives you more flexible payment options. Merchant cash advances let you adjust payments based on daily credit card sales — this helps when business slows down.

The convenience comes at a price though, as annual percentage rates (APRs) can reach 100–200%.

Avoiding common financing mistakes

Many restaurant owners struggle with accurately calculating their break-even points.

Realistic financial forecasts can help prevent this issue by giving a clear picture of when the business will start turning a profit.

Without proper planning, running out of funds too early becomes a significant risk.

Relying on just one source of funding is also a dangerous approach. Diversifying your funding options provides more flexibility and can lead to better terms.

Furthermore, regular consultations with financial professionals ensure you stay on track with tax obligations and avoid potential legal pitfalls.

How OysterLink Supports Your Financial Planning and Growth

A restaurant's financial success hinges on making smart funding decisions.

Owners who understand their financing options and prepare thoroughly are better positioned to secure favorable terms and maintain stable operations.

Savvy restaurant owners take the time to assess a variety of funding sources, from traditional bank loans to alternative financing options.

Building a well-organized financial record and a strong business credit profile opens the door to better lending terms and more funding opportunities.

To ensure both short-term liquidity and long-term stability, restaurant owners should combine professional advice, in-depth research and thoughtful financial planning.

Platforms like OysterLink provide valuable tools and resources to help owners navigate financing options, making it easier to grow and succeed in this competitive industry.

The Fastest Growing

Restaurant & Hospitality Job Platform

Looking for top paid jobs? Or Hiring for your business?

Written by Sasha Vidakovic

Sasha is an experienced writer and editor with over eight years in the industry. Holding a master’s degree in English and Russian, she brings both linguistic expertise and creativity to her role at OysterLink. When she's not working, she enjoys exploring new destinations, with travel being a key part of both her personal and professional growth.

Loading comments...